The explosive growth of peer-to-peer exchanges and emergence of hundreds of alternative digital assets has spurred the interest of both economists and practitioners in cryptocurrency markets. On the surface, the idea of cryptocurrencies as financial assets seems at odds with the conventional wisdom that they represent peer-to-peer methods of payment with the potential to disrupt existing monetary systems, similar to how the internet disrupted standard offline commerce. However, investment value and medium of exchange are two aspects which are inherently interlinked. The intrinsic value of a virtual currency crucially depends on its diffusion as a method of payment and the fact that it attracts market operators with possibly different trading motives.

In this report, we investigate the properties of the aggregate cryptocurrency market across two key dimensions. First, we construct an aggregate value-weighted market index and calculate both the exposure to market risk of cryptocurrencies (i.e. the CAPM beta), and the residual unexplained returns (i.e. the Jensen's alphas). For the main empirical analysis, we utilise a time series of the top 300 cryptocurrencies traded between Dec-13 to Mar-19, on a daily basis. We use daily close prices, trading volume and market capitalisation to construct indexes that are both value- and volume-weighted.

The panel is unbalanced, meaning that the number of cryptocurrencies at the beginning of the sample is not the same as at the end of the sample. Table 1 provides initial descriptive statistics for the top 20 cryptocurrencies.

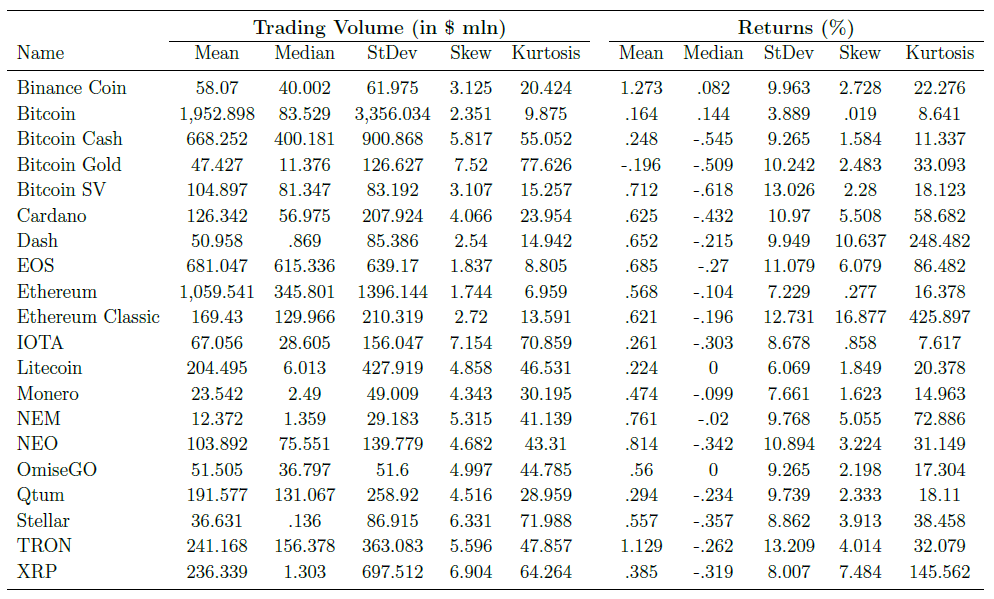

Table 1: A First Look at the Cryptocurrency Market

Table 1 reports a set of descriptive statistics for the daily trading volume, expressed in $mln, and the daily returns in %. For the ease of exposition, we report the statistics for the top 20 cryptocurrencies in terms of market capitalisation over the sample period of Dec-13 to Mar-19. The first five columns report descriptive statistics for trading volume. The picture that emerges is rather clear. Bitcoin (BTC) and Ethereum (ETH) show the highest average trading volume, with daily transactions that amount to almost $2bn and $1bn, respectively. Similarly, BTC and ETH show the highest volatility for market activity, with standard deviations of trading volume far higher than other cryptocurrencies such Litecoin, NEM, Monero, and NEO, to cite a few.

The last five columns report the descriptive statistics for the daily returns. More mature cryptos, such as BTC and ETH tend to show lower returns and volatility. Interestingly, all cryptos show positive skewness and a high level of excess kurtosis over the sample period. This shows that a simple buy-and-hold strategy fully invested in cryptos it is more likely to experience large gains vis-a-vis large losses, even though the latter can be substantial. The massive kurtosis that characterise the distribution of daily returns shows that a simple Gaussian framework cannot capture the time-series variation of cryptocurrency returns. Non-normality has been shown by academic research to be a critical feature for the econometric modelling of cryptocurrency returns.

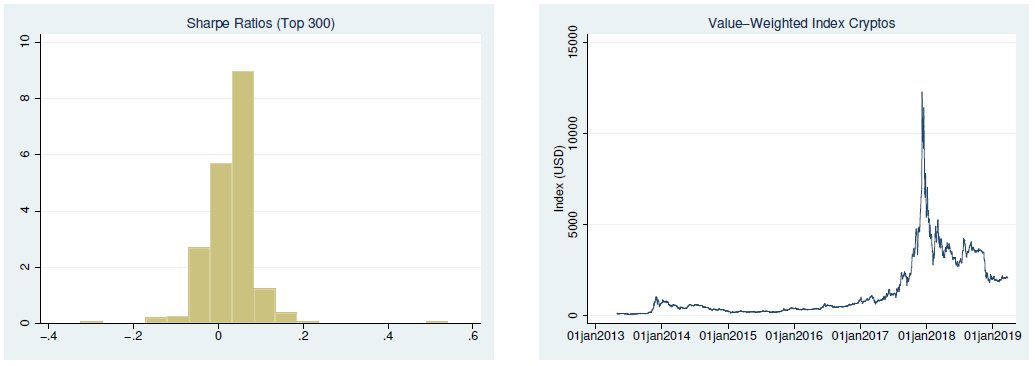

Figure 1: Sharpe ratios and Crypto index of top 300 cryptocurrencies

The left panel of Figure 1 reports the distribution of the Sharpe ratios for each crypto in the sample. The average Sharpe ratio obtained over the sample is equal to 0.032 on a daily basis. The range of possible Sharpe ratios span from a minimum of -0.32 to a maximum of 0.55, again on a daily basis. The vast majority of cryptocurrency deals turned out to generate positive Sharpe ratios (see left panel of Figure 1). The right panel of Figure 1 shows the value-weighted index calculated based on the daily close prices and the relative market capitalisation of each crypto over the sample. The dynamics are quite consistent with the conventional wisdom of a boom-bust cycle of cryptocurrencies between the end of 2017 and the beginning of 2018. However, cryptocurrency markets did not entirely lose their value and have traded laterally from mid-2018 until now.

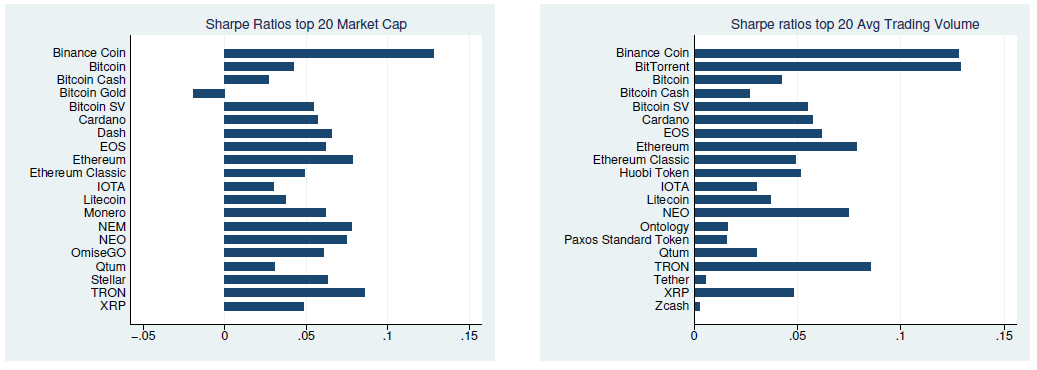

Delving further into the properties of risk-adjusted returns, we now filter the Sharpe ratios by simply looking at the largest and most liquid cryptocurrencies in the sample. That is, we investigate risk-adjusted returns by implicitly controlling for size and liquidity. The left panel of Figure 2 shows the unconditional Sharpe ratios for the top 20 cryptos in terms of average market capitalisation over the sample period. With the only exception of Bitcoin Gold, all Sharpe ratios are in positive territory.

Figure 2: Sharpe ratios of cryptocurrencies

By filtering out for trading volume (i.e. liquidity), the picture slightly changes. The right panel of Figure 2 shows that liquid cryptos tend to have high risk-adjusted returns. This is above and beyond the market size; for instance, BitTorrent is not in the top 20 but still shows a massively positive Sharpe ratio. However, at a general level, the largest cryptocurrencies tend to be the most liquid, as can be seen by looking at the composition of the graphs.

Cross-Sectional Analysis

We now investigate the cross section of the returns of the top 300 cryptocurrencies in excess of their exposure to market risk. The latter is approximated by the value-weighted aggregate market index as shown in the right panel of Figure 1. We regress the returns on each cryptocurrency on the log-returns of the market factor:

where r is the log-returns for a given crypto at time t, alpha is the so-called Jensen's alpha, beta represents the “market beta", and x represents the returns on the value-weighted market portfolio. The estimates of the parameters are corrected for the presence of outliers, as well as autocorrelation and heteroskedasticity in the residuals.

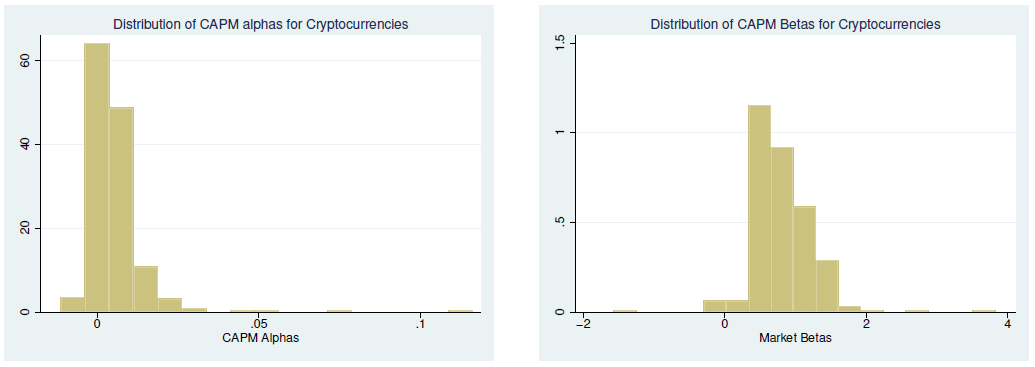

Figure 3: Cross section of alphas and betas of cryptocurrencies

The left panel of Figure 3 shows the cross-sectional distribution of the CAPM alphas for each crypto. Consistent with Figure 1, the risk-adjusted returns of currencies are positive for most of the sample, although to a lower extent than by simply looking at raw Sharpe ratios. The right panel shows the exposure to “market risk", that is, the cross-sectional distribution of the estimates beta, i = 1, ..., N. The exposure to the aggregate market factor is mostly positive in the cross section. Interestingly, the cross-sectional average of the market beta is close to one, which is consistent with the theoretical predictions of a typical CAPM setting.

Market Indexes

We now delve further into the dynamics of cryptocurrency markets by investigating the effect of market size, liquidity and dominant players (BTC in particular) for the dynamics of market returns.

Volume-Weighted Index

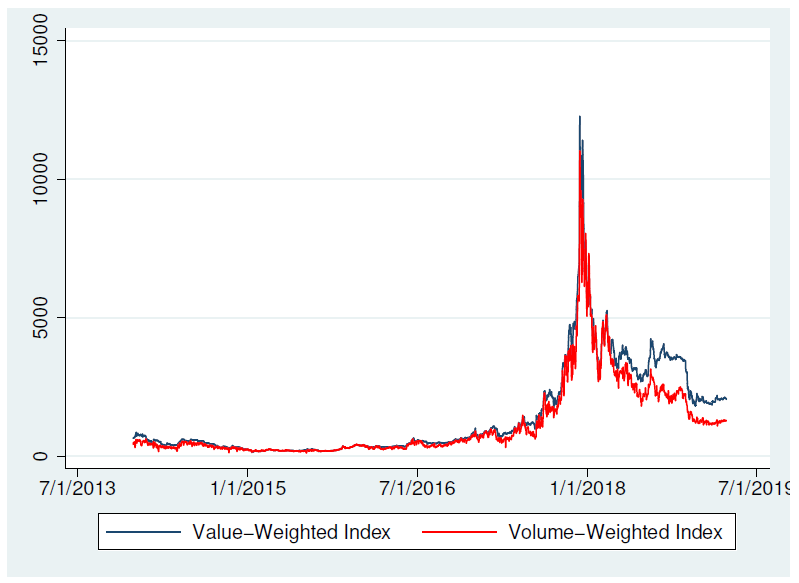

First, we investigate whether market size plays a role in the construction of the market index. In order to do so, instead of value weighting we construct a volume-weighted index, whereby the weight in the index of a given currency for a given day is proportional to its trading volume relative to the aggregate market activity. Figure 4 shows the value-weighted market index (blue line) relative to a volume-weighted market index (red line).

Figure 4: Value and volume-weighted crypto indexes

The figure clearly shows that there is a marked difference in the dynamics of the two indexes after the bubble burst of early 2018. In particular, the volume-weighted index is substantially lower than the value-weighted market index, indicating a significant slow-down in the market activity as proxied by daily trading volume.

Market Indexes Filtering for Liquidity and Size

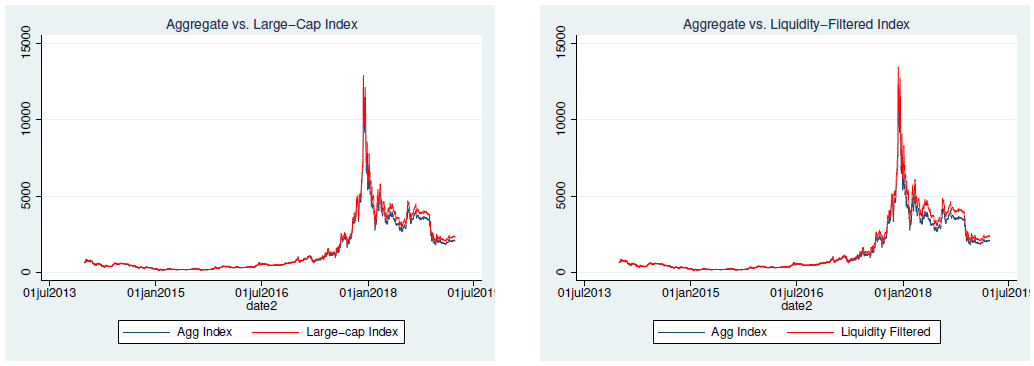

Conventional wisdom posits that the cryptocurrency market is highly concentrated around a few coins. In order to investigate the effect of market concentration on the dynamics of aggregate returns, we now construct two different indexes by filtering for both size and liquidity effects. We first calculate a value-weighted index composed of the top 20 cryptocurrencies in terms of market capitalisation. The left panel of Figure 5 shows the original value-weighted market index (blue line) and large-cap index (red line).

Figure 5: Market indexes of large cap vs market

At a general level, the left panel of Figure 5 provides evidence of substantial market concentration. That is, by focusing only on the top 20 large-cap cryptos, one can effectively track the overall market. This is in line with the conventional wisdom that by trading on the major cryptocurrencies an investor is effectively exposed to aggregate market risk.

In addition, we construct a liquidity-filtered market index which focuses uniquely on the top 20 cryptocurrencies in terms of average trading volume. Specifically, we select the 20 cryptos with the highest average trading volume over the sample period and construct a value-weighted index. This should filter out for low liquid cryptos. The right panel of Figure 5 shows the aggregate value-weighted index and the liquidity-filtered counterpart. Again, it is rather clear the overlapping is almost perfect, in the sense that a dollar spend in a value-weighted market portfolio would generate the same cumulative returns of a value- weighted portfolio which focused only on the most liquid cryptos. This result, coupled with Figure 4, effectively shows that the mismatching between value-weighted and volume-weighted indexes after early 2018 likely comes from the less liquid cryptos.

Market Indexes Without Bitcoin

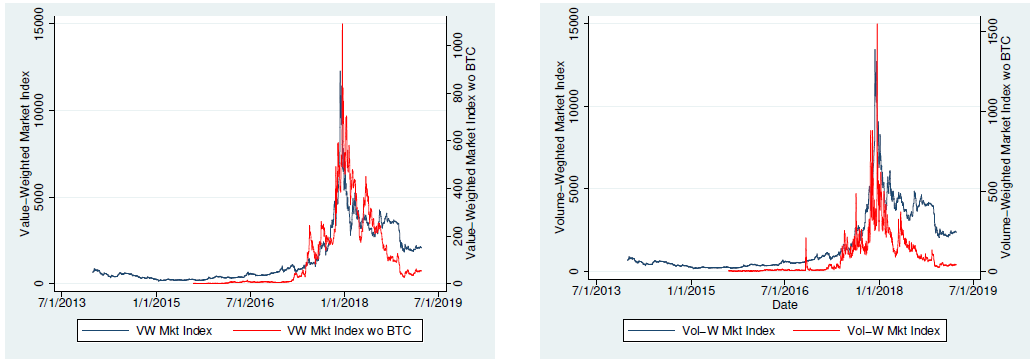

Finally, we investigate the role of Bitcoin, which is akin to the US dollar in traditional currency markets, for the dynamics of cryptocurrency returns. We re-construct all of the above indexes without including BTC in the pool of cryptocurrencies.

Figure 6: Market indexes with and without bitcoin

The left panel of Figure 6 shows the previously calculated value-weighted market index but without including BTC in the set of cryptos. By looking at the scale of the market index without BTC it is evident there is a massive difference in the aggregate value of the index. This is somewhat expected given that BTC has historically always had the highest dollar value in the cryptocurrency markets. Interestingly, not only the magnitude but also the dynamics of the indexes differ. The market crash tends to be much more pronounced by excluding BTC from the set of cryptos. This implicitly means that, despite the massive devaluation, BTC still kept its value much better than other cryptocurrencies, even comparable in terms of market size.

The right panel shows the volume-weighted index with (blue line) and without (red line) BTC. Again, there is a substantial difference not only in the magnitude of the index but also in the dynamics. The market crash is much more pronounced by excluding BTC from the set of cryptos used to construct the index.

As a whole, Figure 6 shows that (1) BTC, being a dominating player, had, and still has, a major effect on the dynamics of cryptocurrency returns, and (2) such effect turned out to be more prominent in the aftermath of the aggregate market collapse of early 2018.

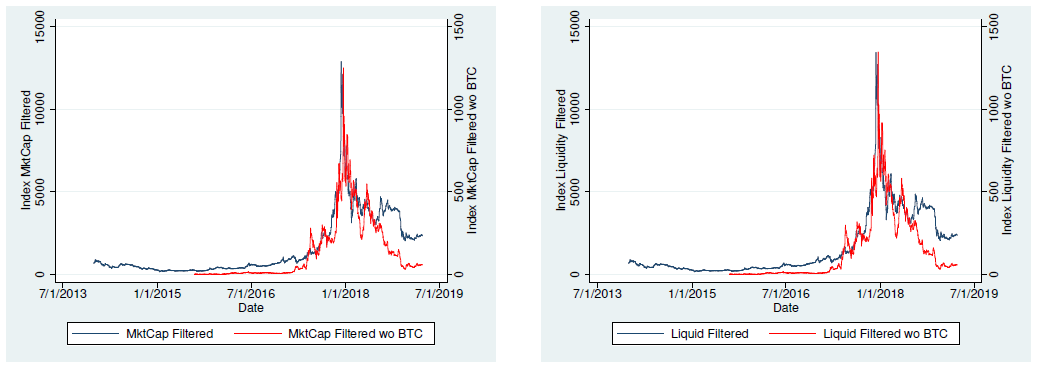

We replicate the same analysis for the large-cap and the most-liquid market indexes. These indexes are constructed as above, that is by selecting either the top 20 cryptos in terms of average market capitalisation or trading volume, but now discarding BTC from the pool of cryptos used to construct the index.

Figure 7: Top 20 crypto market indexes with and without bitcoin

Figure 7 shows the large-cap index with (blue line) and without (red line) BTC. The results of Figure 6 are confirmed (see left panel). BTC plays a major role regardless we are focusing on large caps (left panel) or the most liquid cryptos (right panel). Again, for both indexes the role of BTC turned out to be particularly relevant in the aftermath of the aggregate market collapse of early 2018.