In modern economies, money is created in a joint public-private venture. Banks create the largest share of it as electronic deposits, with around 80% of money in the economy created in this way. Banknotes and coins only make up a small fraction of the total, while the rest is held in reserves at central banks. Despite this, central banks and governments maintain a key role in the management of money. They do this by setting the policy rate (and shaping the yield curve), imposing regulations on banks, supporting payment systems and ultimately providing fiscal backing to the currency if needed.

In the past, private money unbacked by fiscal authority (i.e. the free banking era in the US, 1837-1883) almost universally failed. This is primarily because a privately issued currency faces problems with dynamic instability. If people believe that, in the future, others will not accept private money in exchange for goods, it suddenly loses transaction value. Conversely, a government can guarantee the value of a currency by obtaining real resources through taxation and committing to purchase its own currency, hence putting a hard cap on the price level.

The causes of past failures may be less relevant today due to the emerging properties of cryptocurrencies. They can be used for large international transactions or evade capital controls in a way that is not currently possible with national money.

Brunnermeier et al (2019)1 argue that new currencies are likely to emerge from global social and economic platforms having control over the data - the interactions and transactions - of their users.

Digitalization and the rise of private digital currencies is revolutionising money and payment systems. The advent of these new monies has the potential to induce currency competition between private and government-issued money and reshape the architecture of the international monetary system.

Currency Competition

Competition among private and national currencies is not a new phenomenon. In 1976, in his essay on “Denationalism of Money: An Analysis of the Theory and Practice of Concurrent Currencies”, Hayek observed that national governments have been historically prone to the mismanagement of national currencies. He proposed to replace those with a variety of privately issued currencies competing in a market of monies.

Traditionally, money is an asset that acts as a (i) unit of account, (ii) store of value, and (iii) universal medium of exchange. Each of these three roles emerged in response to different economic frictions:

- Units of account respond to the issue of tracking the relative prices of multiple distinct goods in an economy.

- The need for a store of value arises from the problem of economic agents in coordinating on and committing to future transfers of value.

- The medium of exchange role is a response to the double coincidence of wants: in a barter economy, two economic agents can trade only if each places value on a good of the other.

Currency competition can be of two types. Under reduced competition, monetary instruments denominated in the same unit of account compete in their role as a medium of exchange. This is a common form of competition, encouraged by regulators to enhance efficiency in payment systems. For example, cash, deposits issued by banks, and tokens in digital wallets all denominated in the same currencies all compete as a medium of exchange (and possibly store of value). Under full competition, as proposed by Hayek, currencies can compete also in their role as a unit of account. The competition takes place between monetary instruments denominated in different units of account, each related to a specific price system and inflation rate. This form of competition can happen internationally, among national currencies.

The fundamental issue with Hayek’s proposal is that the unit of account role of currencies has naturally strong network externalities. This forces agents to coordinate on one or very few unit systems. In fact, traditionally it would have been complicated to quote prices and trade in one currency when the prevalent unit in an economy is a different one. Also, switching costs among payment systems using different units generates network externalities, making unit systems more stable over time.

Digital currencies supported by large platforms are likely to make this issue less relevant by lowering the economic frictions giving place to network externalities. For example, they make switching costs very small and allow for instantaneous conversion of different units.

Two deep structural transformations are likely to happen under the currency competition brought about by digital currencies:

- First, the unbundling of the traditional functions of money – store of value, medium of exchange, and unit of account – due to the lower frictions. This will make the competition among currencies much fiercer.

- Second, the competition among digital money issuers will push them to re-bundle monetary functions with traditionally separate functions, such as data gathering and social networking services, in order to product-differentiate their currencies.

Emerging Platforms

Digital money has gained a role in many different environments. For example, WeChat’s and Alipay’s digital wallets dominate the payments system in China, while Safaricom’s M-Pesa has a large role in transfer services in Africa. However, Facebook’s project of Libra, a “stable coin” pegged to a basket of currencies and assets, has true transformative potential.

Large platforms like Facebook have unparalleled access to user data both in terms of size (up to billions of users) and depth (their behaviours and beliefs). Such platforms are natural “ecosystems” in which consumers, merchants, and service providers interact and trade. Different platforms could provide different bundles of money and data services associated with platform-specific digital payment instruments.

Digital connectedness can reshape the geography of distances among platform users and supersede the importance of location and macroeconomic links. This could lead to the rise of “Digital Currency Areas” (DCAs), connecting a digital currency to a community of users of a particular digital network.

This dynamic would make both emerging and advanced economies vulnerable to a new form of dollarization, a “digital dollarization”, in which the national currency is superseded by a platform’s currency rather than another country’s currency.

How can a government retain monetary authority when challenged by digital dollarization? A Central Bank Digital Currency (CBDC) is a natural way to grant the general population direct access to public money, and maintain the uniformity of money in a digital economy and hence its nature as a public good. In fact, convertibility of deposits and digital currencies into CBDC would restore substitutability and uniformity across payment instruments.

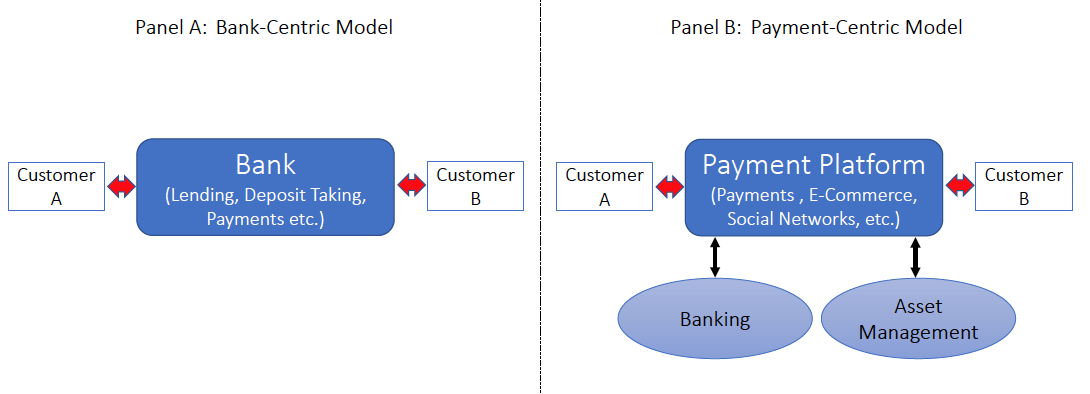

Figure 1: The Architecture of the Financial System

In modern economies, banks are at the very centre of the financial system (i.e. they provide the means for consumers to store and exchange value). Most transactions happen through banks, and economic agents transact via bank operations. Payment systems are at the margins of the network.

Platforms have to potential to reshape financial systems. In fact, the platform would organise other activities around the central payment functionality. Other financial services such as credit and insurance would be functionally subordinated to payment services.

Crypto-enforced Monetary Policy Synchronization

Benigno et al (2019)2 discuss the international implications of the emergence of digital currencies, in a more formal two country model featuring a home, foreign and global (crypto)currency all providing liquidity services.

In the benchmark case in which markets are complete, liquidity services are rendered immediately and the global currency is adopted globally, they show that nominal interest rates must be equal and the exchange rate is risk-adjusted martingale. This full synchronization of the two monetary regimes is called by the authors a “crypto-enforced monetary policy synchronization” (CEMPS).

What could the central bank do to regain monetary independence? It could adjust interest rates down or up relative to the foreign interest rate. By lowering the risk-free interest rate in the home currency below that in the foreign currency, the central bank lowers the opportunity costs of holding the domestic currency. This makes it more attractive than the global currency as a means of payment, crowding out global currency in its own country. Yet nominal interest rates can only be lowered to zero, hence currency competition between the two countries would trap both the economies at the zero lower bound. By increasing the risk-free rate, instead, the central bank risks that its own national currency is abandoned as a medium of exchange.

Moreover, if the global currency is backed by interest-bearing assets, additional and tight restrictions on monetary policy arise. In fact, by selecting appropriately low and competitive fees, the global currency consortium can force both economies to the zero lower bound.

These results propose a strengthened version of the Mundell-Fleming Trilemma or Impossible Trinity. The Trilemma states that is impossible to ensure at the same time a fixed exchange rate, free capital flows, and an independent monetary policy. When a global cryptocurrency comes into play, monetary policy independence is lost even when exchange rates are flexible and capital flows free.

Conclusion

The rise of cryptocurrencies has the potential to radically reshape the money space and the whole financial system. It can do this by unbundling the three roles of money, creating competition among national and private currencies, and then combining money and payment services with data services in systemic platform ecosystems. This will have important implications on data regulation, the banking sector and even central bank independence.

Digital currencies have the potential to transform the international monetary system. Large platforms issuing digital currencies may create a “digital currency area”, posing a new threat to the established currencies of both emerging and advanced economies. A harsher Trilemma may emerge – if a global cryptocurrency comes into play, monetary policy independence may be lost even under flexible exchange rates and free capital flows.

Bibliography

1 Markus K. Brunnermeier, Harold James, and Jean-Pierre Landau, “The Digitalization of Money” (NBER working paper)

2 Pierpaolo Benigno, Linda M. Schilling, and Harald “Cryptocurrencies, Currency Competition, and the Impossible Trinity” (NBER working paper)