How should public blockchains be governed? Bitcoin and Ethereum use a more informal approach, where decisions are made using consensus and off-chain negotiations. Other blockchains, such as Tezos and Decred, implement a formal governance model with explicit rules and anonymized, on-chain voting. In this note, we describe both approaches and examine their pros and cons.

The issue of how to govern a blockchain has been steadily growing in importance over the years, as more projects take off and the ones that succeed attract a lot of users and create significant value. The earliest and most well-known blockchains, such as Bitcoin and Ethereum, implement an informal governance structure, where the key stakeholders meet off-chain and reach consensus on how the project should proceed. On the other hand, newer blockchains, such as Decred and Tezos, try to emphasize that their comparative advantage is “good governance”, implemented through a formal model of explicit rules and anonymized, on-chain voting. In this note, we describe both approaches and examine their pros and cons.

Informal Governance

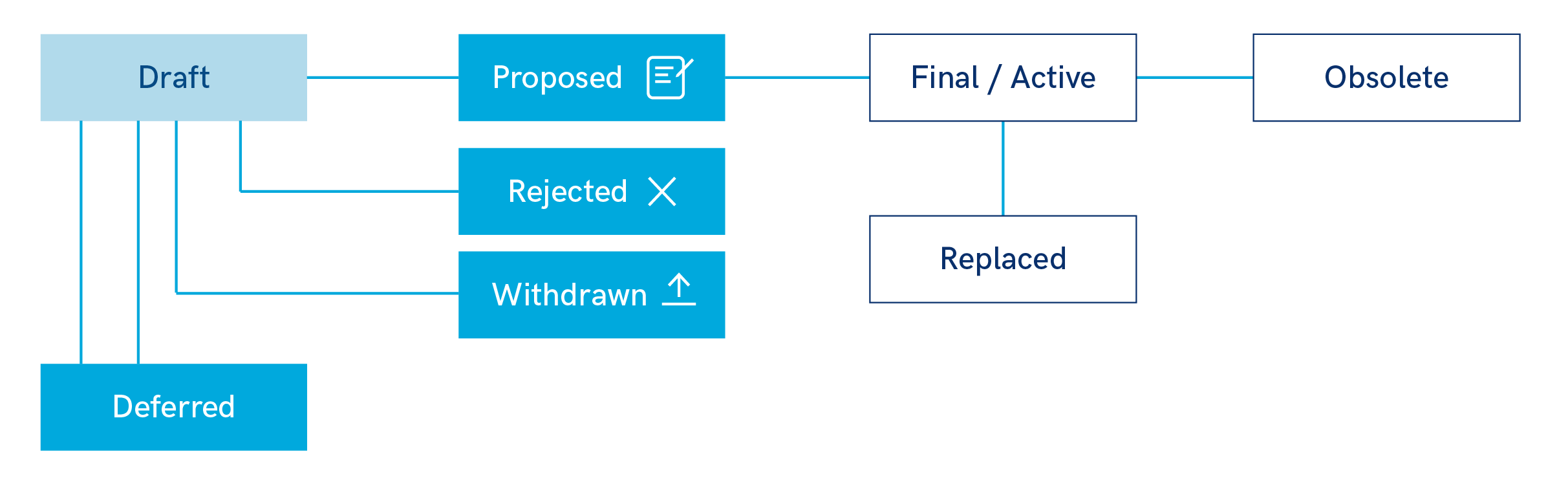

The two most well-known Blockchain networks, Bitcoin and Ethereum, implement an informal governance structure, using the Bitcoin Improvement Proposals (BIPs) and Ethereum Improvement Proposals (EIPs) platforms, respectively.1 Changes are first suggested and then discussed by the wider community of stakeholders (developers, miners and users). Decisions on whether to accept, defer or reject a proposal are made using consensus. The graph below shows the typical lifecycle of a Bitcoin Improvement Proposal.

Figure 1: Lifecycle of a Bitcoin Improvement Proposal

The advantage of deciding through consensus is that, at least in theory, it enables anyone to participate, thus serving one of the main desiderata of public blockchains, which is decentralisation. However, consensus building may be a non-transparent procedure among a few key participants, leading in practice to a more centralised system.

Consensus and Forks

If consensus cannot be reached, the blockchain may split through forking. A fork occurs when two separate and parallel chains are created, which differ in terms of the state of the blockchain. For example, they may contain a different set of transactions, or they may implement a different rule, such as the permitted size of each block. Users then informally “vote” on the proposed changes, by choosing which chain to follow.3 Their choice does not depend only on what they think is best for the blockchain, but also on which chain they think others will follow. In other words, there are network effects, because as more users follow a particular chain, the associated cryptocurrency becomes more valuable. Another complication arises from the fact that cryptocurrency exchanges only list a small number of currencies, which makes it difficult for a minority group to maintain a chain that is not followed by a critical mass of users, even if they consider it to have a better design.

Lee et al. (2020) use these observations to analyse blockchain governance, through a model of electoral competition. A participant first proposes a new state for the blockchain, hence creating a hard fork. Then, all other participants vote by choosing to follow the new chain or stay on the old one. This is similar to a well-known model, first analysed by Hotelling (1929) and Downs (1954), with two political parties that propose competing platforms and voters choosing between the two. The main result of this literature is the Median Voter Theorem, which specifies that the winner is a platform that is closest to the median voter’s ideal policy.4 In other words, moderate policies are favoured. However, Lee et al. (2020) show that this result is no longer true here, exactly because of the network effects and the negative impact of cryptocurrency exchanges on minority chains. Under some conditions, a radical change of the status quo is more preferable than a moderate change and it is implemented through a fork. In that case, both chains survive.

Lee et al. (2020) use their model to explain the famous split of Bitcoin, that occurred in 2017. There was a proposal to increase the block size of Bitcoin, to allow a greater number of transactions per block and decrease the miners’ fees. This proposal was rejected by the core developer team, leading a substantial number of developers and miners breaking away and creating Bitcoin Cash. Before 2017, there were several more moderate proposals to increase the block size, but they were rejected and there was no split. In 2018, there was a further split between Bitcoin Cash and Bitcoin SV.

Formal Governance

The aim of formal governance is to provide a more transparent and efficient decision-making process, also avoiding the need for hard forks. It is implemented by embedding specific rules in the system, which can only be changed through formal procedures, such as voting.

Tezos is a blockchain network that implements a Proof-of-Stake mechanism, that aims to avoid splits in the blockchain through self-amendments.5 As with informal governance, stakeholders submit proposals for amendments, which are discussed and tested by the network. The difference is that changes are implemented only if they have the support of the majority, which is expressed through on-chain voting, called liquid Proof-of-Stake. As with any Proof-of-Stake protocol, participants stake their coins in order to be selected to create the new blocks of transactions, so that they get rewarded.6 In Tezos, however, their stake also provides them with proportional votes, that they can then use to approve or reject changes. Participants can either vote directly or delegate their votes to others. Decred is another blockchain network that uses delegated voting, which is achieved by purchasing tickets, which are then used for voting.7

In both systems, voting power is proportional to the value they "invest" in to become an influential voter. Incentives are in theory aligned as the most influential voters stand to gain the most from good decisions which benefit the platform and other users, but also stand to lose the most if the decision causes harm.8 Both these networks implement a “fluid” delegation system, because any voter can create or withdraw delegates quickly. In other protocols, delegation is more rigid. For example, in EOS, 21 block producers govern the blockchain with consensus, but they are voted by the stakeholders using their EOS tokens.9

Although formal governance promises an efficient and transparent decision-making process, it has several drawbacks.10 First, the blockchain network can be centralised if there is low voter participation, or there is wealth inequality, such that very few participants control most of the votes. Low voter participation has been observed in several networks and can easily be explained. A stakeholder incurs a cost (in terms of time and effort) to understand the proposed changes and vote. However, the probability that the voter will be pivotal, i.e. that they can influence and change the result, is minimal. Therefore, it is rational for them to abstain from voting in order to avoid the cost and free ride, hoping that others will vote correctly. This consideration can also lead to bribes. For example, an exchange can offer attractive rates for lending the cryptocurrency, then using the deposits as stakes, in order to win votes and influence the direction of the project.

Finally, it is often difficult to formalise a process that is flexible enough to be optimal for all possible contingencies. In that sense, off-chain human interaction and consensus building is often indispensable.

Conclusions

Formal and informal governance encompass a variety of protocols, with both pros and cons. Unfortunately, no protocol is completely immune to being taken over and centrally managed by a powerful minority. Protocols that implement informal governance seem to be more flexible and benefit from allowing direct human interaction, whereas those with formal governance are more transparent and can be more efficient at resolving disputes, without the need for forking. Although we cannot expect that there will be a one-size-fits-all design for all blockchains, it is more likely that a hybrid system will prevail, as it is the case with the governance of democracies and companies, which combine both formal elements, such as voting, and informal elements, such as consensus building within a government or a board of directors.

Bibliography

Buterin, V, 2019. Notes on Blockchain Governance.

Downs, A., 1957. An Economic Theory of Democracy, New York: Harper and Row.

Hotelling, H., 1929. Stability in Competition. Economic Journal, 39, 41–57.

Lee, B.E., Moroz, D.J. and Parkes, D.C., 2020. The Political Economy of Blockchain Governance. Available at SSRN 3537314.

Footnotes

1 More information about the Bitcoin Improvement Proposals can be found at https://en.bitcoinwiki.org/wiki/Bitcoin_Improvement_Proposals and for EIP at https://eips.ethereum.org/. Both are derived from the Python Enhancement Proposals, where proposed changes are informally discussed and reviewed by the community of developers utilising the IRC channels, and Github.

2 For more information on Bitcoin Improvement Protocols, see https://en.bitcoinwiki.org/wiki/Bitcoin_Improvement_Proposals

3 There are two types of forks. A soft fork means that there is backward compatibility: any element of the old version can be accessed and read by the new version of the blockchain. A hard fork implements a more severe break, as there is no backward compatibility.

4 The median voter’s ideal policy is both below and above the ideal policies of 50% of the voters.

5 The consensus protocol used is Nakomoto Consensus, or longest chain rule. See An Introduction to the Distributed Ledger Technology for more information.

6 See An Introduction to the Distributed Ledger Technology for more details on the Proof-of-Stake protocol, which is an alternative to the Proof-of-Work protocol.

7 A summary of the drawbacks of formal governance is provided by Buterin (2019).

8 This approach also creates resistance from Sybil attacks, which is the primary concern for decentralised systems without a central authority governing it. In such systems one user one vote is not enforceable.

9 For more information on delegated Proof-Of-Stake and EOS Delegates, see https://coincentral.com/what-is-an-eos-delegate/.

10 See https://sigilfund.com/research/on-decentralized-governance-and-digital-democracy/ for an interesting analysis of blockchain governance, including a short description of Tezos and Decred.