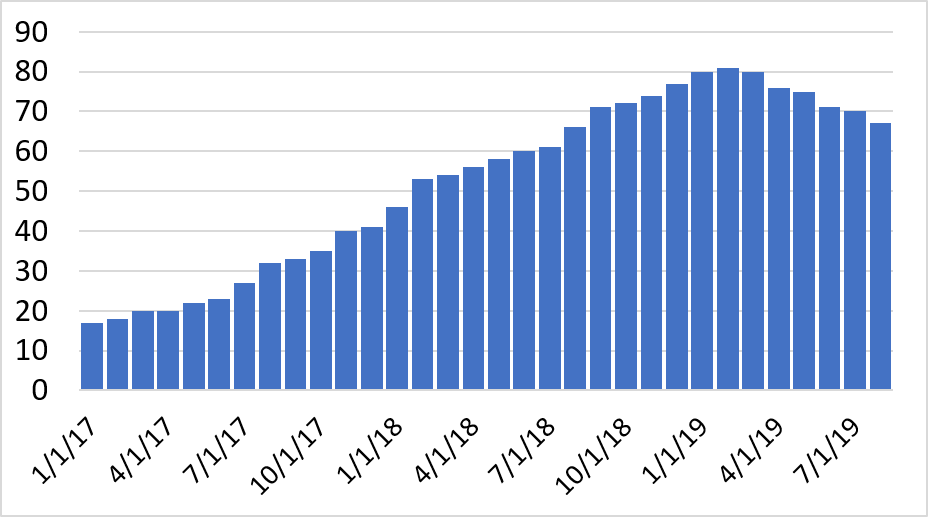

Cryptocurrency funds can take many names: blockchain funds, digital asset funds, tokenised funds. Whatever you may call them, their number has increased exponentially since early 2017 on the back of rising prices and public awareness. For comparison, there were around 20 funds formally reporting performance in our selected sample in January 2017. By August 2019, the number has grown by more than three times. Most of these funds are labelled as Hedge Funds. There are also a handful of so-called “tokenised” funds. The latter can be delivered to investors as a security that can be resold as soon as a year later. Figure 1 shows the number of cryptocurrency funds selected in our sample from January 2017 to August 2019.1 Interestingly, the number of active funds follows quite closely the price dynamics in cryptocurrency markets, with the price run-up in late 2017.

Figure 1: Number of active funds over time

Active management has been the default option for investors looking for external money managers for almost two decades, at least until the first index mutual funds were made available in the late 1970s. In equity markets, the rise in popularity of Index Funds and Exchange Traded Funds (ETFs) has put into question the very existence of mutual funds. This is not the case in the cryptocurrency investment industry, whereby only few passive funds exist. Active portfolio management is dominant in the cryptocurrency space.

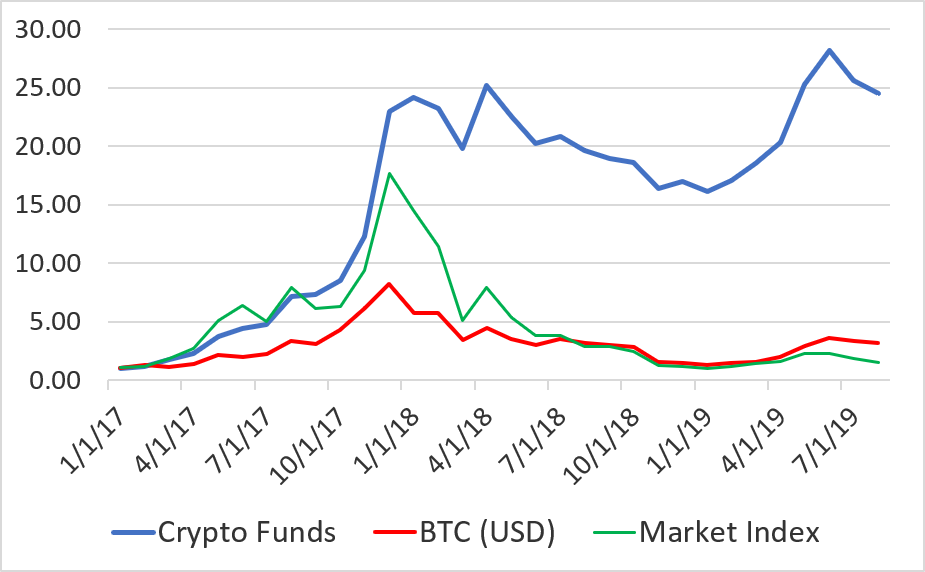

As far as the performance is concerned, crypto funds significantly outperformed Bitcoin and most other cryptocurrencies since early 2017. Figure 2 shows this case in point. We compare the compounded returns of investing one dollar in cryptocurrency funds vis-à-vis the returns on BTC and the wider market. The returns for crypto funds are approximated as an equally weighted index all of the funds included in our sample. The returns on BTC are the returns of BTC/USD pair aggregated over more than 200 exchanges. The market index is a value-weighted index of the top 30 cryptocurrencies by market capitalization.

Figure 2: Compounded returns of cryptocurrency funds

The figure makes a strong case for pooling investment through funds rather than investing directly in cryptocurrencies. Both BTC and the market have underperformed the average cryptocurrency fund. The difference by the end of the sample becomes quite significant: a one dollar investment in cryptocurrency funds would have generated an astonishing 25 dollars towards the end of the sample. On the other hand, investing one dollar directly in BTC and in a panel of large cryptocurrencies would have generated 3.2 and 1.5 dollars, respectively.

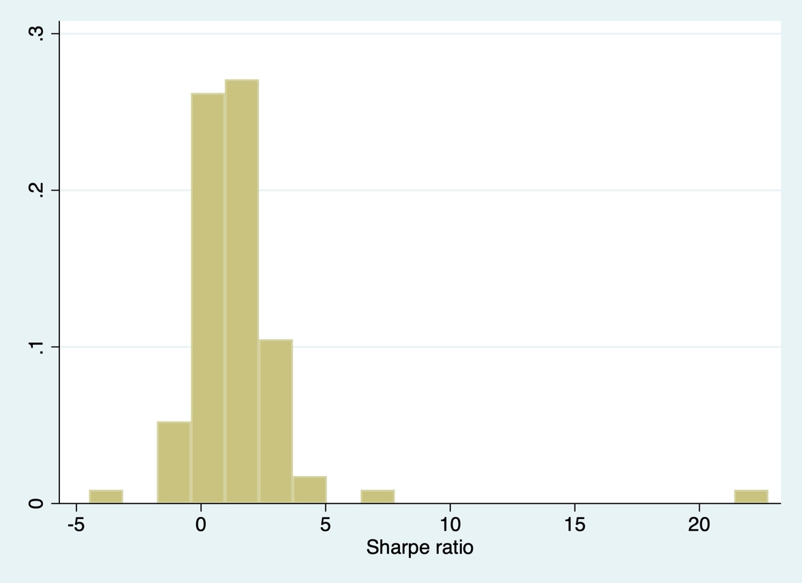

Despite being profitable on average, cryptocurrency funds are not all alike. Figure 3 makes this case in point. The figure reports the cross-sectional distribution of the unconditional Sharpe ratios for each of the cryptocurrency funds. Sharpe ratios are simply calculated as the sample mean of the returns for each of the funds divided by the sample standard deviation. Such a metric is useful to understand the risk-return profile of a fund as it gives the return of a given fund per unit of risk undertaken.

Figure 3: Sharpe ratios of cryptocurrency funds

Two interesting facts emerge. First, there is substantial heterogeneity in the cryptocurrency investment industry in terms of risk-adjusted returns. In fact, not all funds have a good performance, even in unconditional terms, with some investment generating a negative return per unit of risk. Second, there is a considerably higher fraction of funds with Sharpe ratios above vs below average, that is the distribution of SRs is positively skewed. That means that one could pick the most successful funds in order to significantly outperform a simple equally weighted portfolio of funds. Generally, Figure 3 makes the case for a careful screening process when allocating investments to different cryptocurrency funds.

A key aspect of the fund screening process is to understand the risk exposures of different funds. That is, to understand the sources of risks that can explain fund performances. In this respect, the idea is to separate the risk generating process in betas vs alpha, that is returns simply due to exposure to risk rather than actual outperformance. In order to do that, a simple approach is to regress the net returns of each fund on a set of cryptocurrency-specific risk factors.

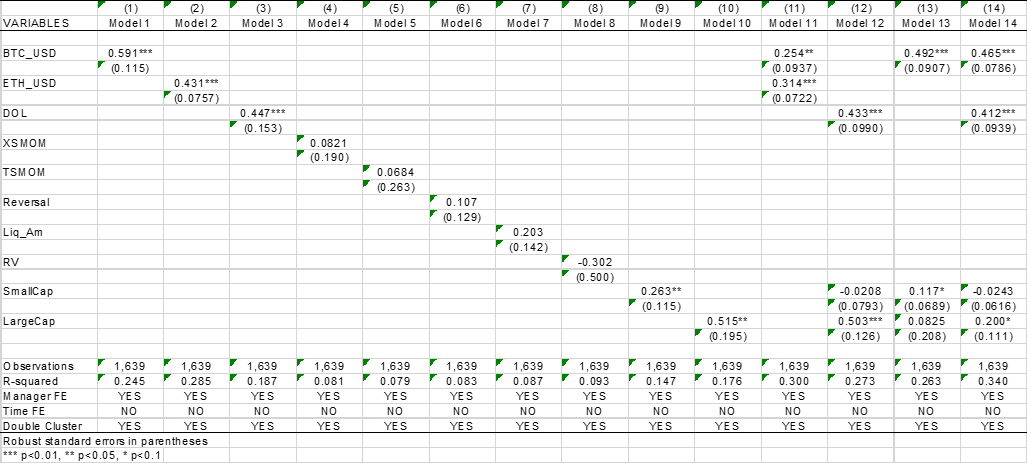

Table 1 reports the results of a panel regression analysis in which the dependent variable is the (net of fees) returns on cryptocurrency funds and the independent variables are a set of cryptocurrency-specific risk factors. We consider a variety of different sources of risk which may be relevant for cryptocurrency investments. First, we consider the simple returns on BTC and ETH (in USD) as factors driving fund returns. The logic is that we want to control for a simple exposure to dominant market drivers.2

Next, we consider the equivalent of a “dollar” risk factor (DOL), calculated as a simple equally weighted average of the top 300 cryptocurrency pairs against the USD (see Lustig et al. 2011 for the FX market). Momentum also represents a common risk factor used in the mutual funds industry to understand returns dynamics. We implement two alternative definitions of momentum: cross-sectional momentum (XSMOM) as in Jegadeesh and Titman (2001) and time-series momentum (TSMOM) as in Moskowitz et al. (2012). The opposite of momentum is a simple reversal strategy which goes long in past “losers” and short in past “winners”. Liquidity and volatility also represent important risk factors when investing in cryptocurrencies; we follow Amihud (2002) and construct long-short mimicking portfolios for liquidity (Liq_Am). Realized volatility (RV) is constructed as a long-short portfolio which goes long in the cryptocurrencies with low volatility (bottom decile) and goes short in those with high volatility (top decile). Finally, we consider both a large-cap index – constructed as a value-weighted average of the top 30 cryptos – and a small-cap index – constructed as a value-weighted average of the remaining 270 top cryptos in terms of market cap – in order to capture some sort of size effect. A detailed description of these risk factors and their construction can be found in Bianchi and Dickerson (2019).

Table 1: Cryptocurrency funds and sources of risk

A few interesting facts emerge: first, there is considerable evidence that crypto funds returns are exposed to a “market” factor, both through BTC and ETH. In addition, a simple equal-weight portfolio is also highly significant. These findings corroborate with the idea that the main source of risk in the cryptocurrency investment space is the market. Second, none of the conventional momentum, liquidity and realized volatility factors seem to play any significant role as far as fund returns are concerned. Third, exposure to small caps, that is cryptocurrencies with smaller market value, turns out to be relevant. However, Model (13) shows that when small-cap and BTC are included together in the same model, the effect of small-cap tends to vanish.

As a whole, Table 1 tells a simple story. That is, it is primarily market risk that can explain cryptocurrency fund returns. An additional comment is in order however. The explained variation, that is the R-squared in the regressions, is around 34% for the most significant model, i.e., Model (14). That means there is a considerable fraction of return variation on average across funds, that cannot be explained by the considered risk factors.

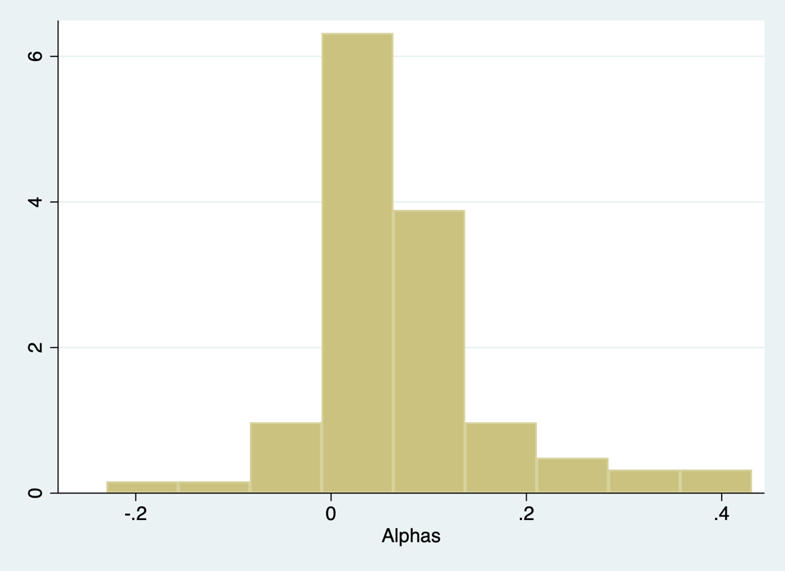

Such unexplained returns could be thought of as the ability of fund managers to generate value, i.e., the so-called Jensen’s alpha. Figure 4 shows the cross-sectional distribution of the alphas.

Figure 4: Alphas for cryptocurrency funds

Two interesting facts emerge. First, there is considerable dispersion in the ability of funds to generate returns in excess of the market, with a considerable number actually underperforming the market. Second, the distribution of alphas seems to be skewed to the right, that is, the fraction of managers outperforming the market is higher than the fraction of managers that underperforming.

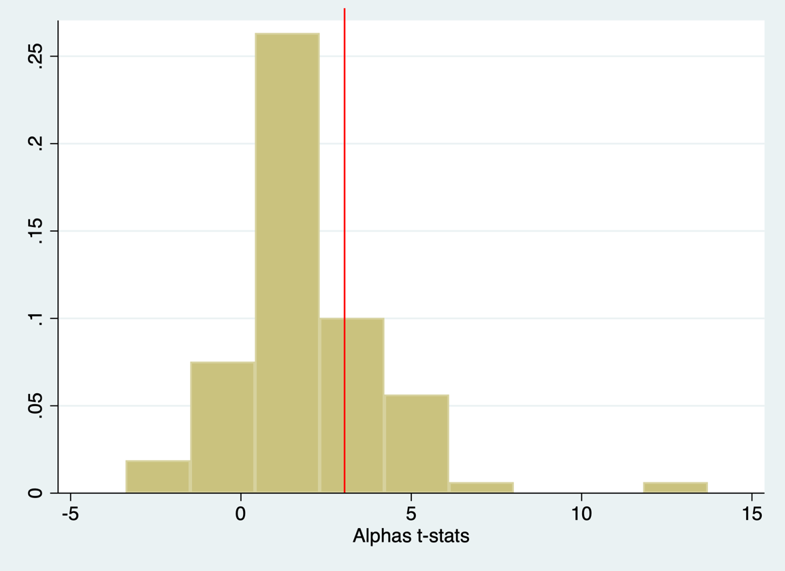

Although the majority of alphas seem to be positive, that does not guarantee that they are effectively statistically different from zero. This is what investors ultimately should care about - picking a fund whose alpha will not be effectively equal to zero if the fund runs long enough. Figure 5 makes this case in point. The figure reports the t-statistics (alpha estimate / standard error) for each of the alphas reported in Figure 4. The red vertical line shows a conventional threshold of 3 which accounts for multiple testing issues (see Harvey et al. 2016).

Figure 5: T-statistics of the alphas for cryptocurrency funds

The fraction of valuable funds is much lower than expected. A simple calculation shows that roughly a third of the funds can generate a performance that is significantly higher than the market. That implicitly means that a careful evaluation of the funds’ actual risk-adjusted performance and a consequential fund-picking strategy can prove to be crucial to avoid paying unnecessary fees and even underperform the market in the medium to long term.

Concluding Remarks

The cryptocurrency industry has been exponentially growing over the last few years due to (1) public awareness, (2) investors in search for yields, and (3) more stable cryptocurrency prices and volatility. The performances of funds are not all alike and, most importantly, they are not all positive on a risk-adjusted basis. This makes fund screening and performance evaluation not only crucial, but consequential for the implementation of a successful and diversified investment strategy.

Bibliography

Jegadeesh, N. and Titman, S. (2001). Profitability of momentum strategies: An evaluation of alter- native explanations. The Journal of Finance, 56(2):699–720.

Amihud, Y. (2002). Illiquidity and stock returns: cross-section and time-series effects. Journal of financial markets, 5(1):31–56.

Lustig, H., Roussanov, N., and Verdelhan, A. (2011). Common risk factors in currency markets. The Review of Financial Studies, 24(11):3731–3777.

Moskowitz, T. J., Ooi, Y. H., and Pedersen, L. H. (2012). Time series momentum. Journal of Financial Economics, 104(2):228–250.

Harvey, Campbell R., Yan Liu, and Heqing Zhu. "… and the cross-section of expected returns." The Review of Financial Studies 29.1 (2016): 5-68.

Bianchi, D. and Dickerson, A. (2019). Trading volume in cryptocurrency markets. Working paper.

Footnotes

1 Notice that the sample size comprises of the top active funds which have been directly verified through an extensive due-diligence process. This explains why the reported universe of funds is smaller than the actual number of available funds in the cryptocurrency space. A more general overview of the industry can be found here https://cryptofundresearch.com/cryptocurrency-funds-overview-infographic/.

2 As of now, the market capitalisation of BTC and ETH combined is around 70% of the total market. That means that these two factors combined should capture most of the variation in total market returns.