On-chain transaction volume refers to cryptocurrency transactions which occur on the blockchain. These transactions are considered to be valid only when the blockchain is modified and the public ledger record is updated. In this respect, on-chain transactions are dependent on the state of the blockchain for their validity.

Although in principle on-chain transactions are supposed to occur in real-time in order to keep the blockchain instantly verifiable and transparent, in reality transactions are completed with delay. As a matter of fact, it takes a random amount of time to accumulate the sufficient number of verifications from miners before confirming a transaction. For instance, if transaction volume is high, a limited number of miners may take their own time to confirm a transaction, making all involved parties wait for a longer amount of time.

On-chain transactions also come at a cost, as miners command a fee when confirming a transaction on the blockchain. At times, this fee can become very high depending on the network’s scalability potential and transaction volume. Nevertheless, on-chain transaction volume offers a somewhat reliable estimate of the underlying value of a cryptocurrency as a mean of transferring resources (i.e. a payment method). As a result, some of the most used crypto valuation methods are directly derived from on-chain transactions.

In this report, we focus on Bitcoin (BTC) and outline some of the main valuation measures based on blockchain transaction fundamentals. These include: the Network-Value-to-Transactions (NVT) Ratio, Network-Value-to-Realised-Value (NVRV) Ratio; the Network-Value-to-Metcalfe’s-Law (NVML) ratio; and the Exchange vs On-chain Trading Volume Ratio.

Network-Value-to-Transactions ratio

The Network-Value-to-Transactions (NVT) ratio measures the dollar value of on-chain transaction activity of a given cryptocurrency network relative to its network value. More precisely, NVT is calculated as the Network Value (total dollar value of all the circulating units of a given crypto asset, equivalent to the market capitalisation of a stock) divided by On-chain Transaction Activity (dollar value of transactions settled on the cryptoasset’s blockchain).

Given that transaction volume can be quite volatile on a daily basis, on-chain transactions are often smoothed by taking the 90-day moving average of the adjusted transfer values expressed in USD.

In simple terms, the NVT can be understood as the dollar amount an investor can expect to invest in a cryptocurrency (e.g. in BTC), relative to the value of one dollar being transmitted on the blockchain. As a result, NVT is often used as a valuation metric. An NVT higher than the historical average suggests that the market is placing a premium on BTC as a method of payment. On the other hand, an NVT lower than its historical average suggests that the market is placing a discount on BTC as a method of payment.

NVT conceptually shows similarities with the standard Price-to-Earnings (P/E) Ratio used in equity markets. Similar to earnings for companies, the amount of value transmitted on the blockchain suggests that BTC is in fact used as a medium of exchange and therefore should represent a key performance indicator. The underlying assumption is that NVT is assumed to fluctuate around some long-run equilibrium value, that is, NVT can be used to understand if BTC is undervalued or overvalued.

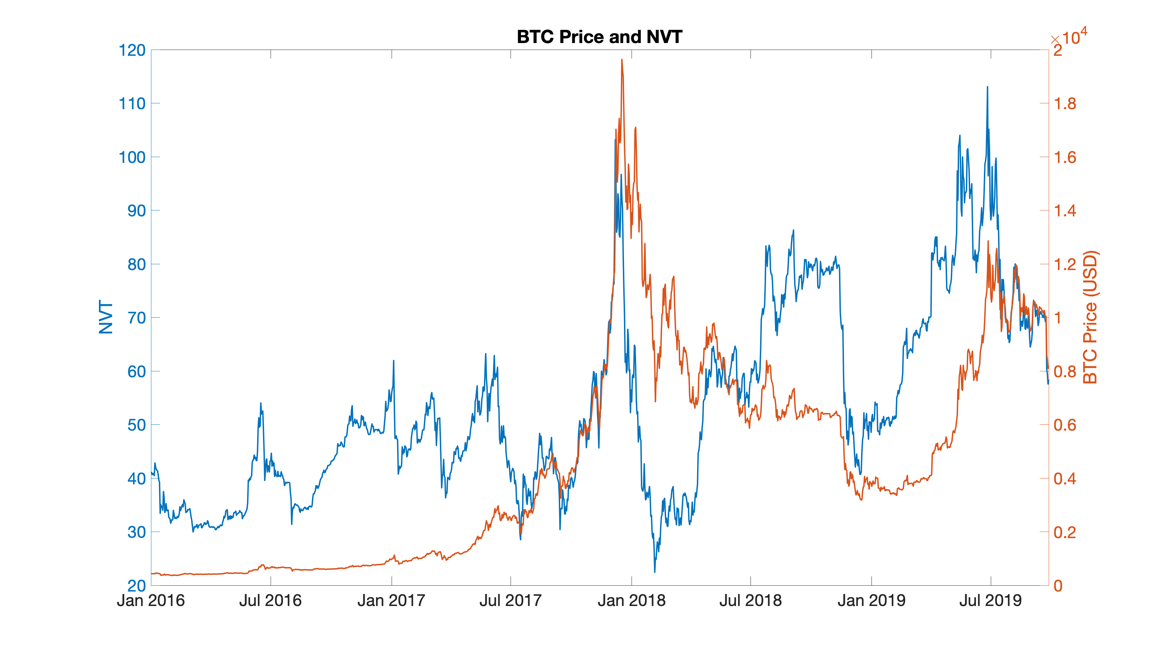

Figure 1: BTC Price and NVT

Figure 1 shows that the NVT tracks somewhat closely the dynamics of BTC prices over time, although with some lag (see for instance the price run up in early 2019). The sharp increase in the BTC price of late 2017 is closely tracked by the NVT. The fact that NVT seems to be a lagging indicator of price changes could put into question the usefulness of it as a trading indicator. Nevertheless, as a valuation indicator, it helps investors understand the value trend of Bitcoin as a transaction medium, as well as the price that the market assigns to this function.

Several recipes exist in terms of constructing trading signals based on NVT. For instance, one strategy is to set both lower and upper thresholds of NVT values such that, once crossed, these signal that BTC is either overbought or oversold. This is very much in the spirit of traditional technical indicators such as the Relative Strength Index (RSI) and the Moving Average Convergence Divergence (MACD).

However, the NVT does have several limitations. For example, it does not take into account trading that is executed on exchanges. The dollar amount traded on exchanges tend to be larger than the dollar value of on-chain transactions. As a result, NVT does not take into account short-term fluctuations due to speculative pressures. This may be outside the “value proposition” of NVT in the first place but is a relevant aspect that should be considered when designing trading algorithms. Also, on a conceptual level the metric could be said to slightly undersell the utility of Bitcoin as a store of value.

Network-Value-to-Realised-Value ratio

The Network-Value-to-Realised-Value (NVRV) ratio measures the dollar value of a crypto asset’s Realised Value relative to its Network Value. More precisely, the NVRV can be calculated as a simple ratio between the Network Value (total dollar value of all circulating units of a given crypto asset) and Realized Value (value of the network, whereby each Bitcoin is aggregated and assigned a price based on the moment when each Bitcoin was last transferred to a new address).

In simple terms, the MVRV can be understood as the relationship between high time preference-related use of BTC (i.e. short duration uses, speculation) over certain periods, vs low time preference-related use of Bitcoin over certain periods (i.e. long duration uses, long-term investors). In other words, it accounts for the length of time Bitcoin has been held by investors – a proxy for its store of value property.

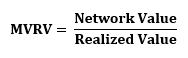

Figure 2: BTC Market Value vs. Realized Value

Figure 2 shows that these two components are not equivalent. The realised value (based on BTC market prices when each coin has been transferred), which is intuitively linked to longer-term uses of BTC (e.g. store of value), is much smoother and unaffected by the bubble burst of early 2018. On the other hand, the market value, which is linked to the short-term uses of BTC (e.g. speculative trading), is more volatile.

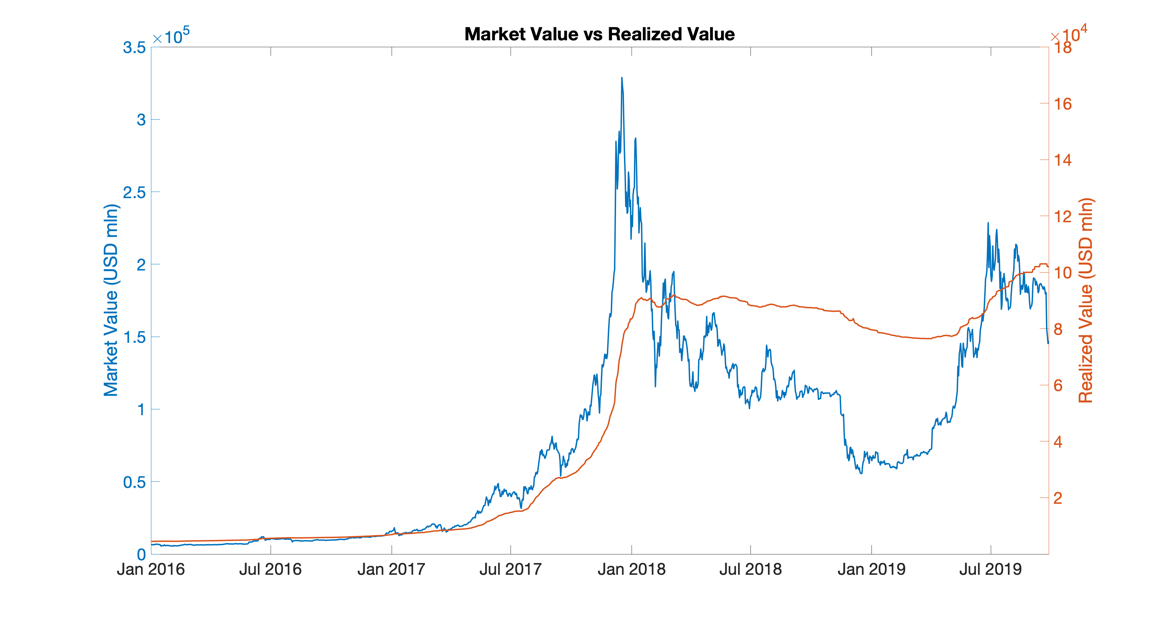

Figure 3: BTC Price and MVRV

All things equal, a higher MVRV than its sample average tends to be associated with a BTC price that is primarily influenced by short-term investors. On the other hand, a lower than average MVRV suggests that the BTC price is primarily driven by long-term investors.

Figure 3 shows that MVRV is closely linked to the dynamics of BTC prices, especially in the aftermath of the bubble burst of early 2018. As a matter of fact, after early 2018 the dynamics of the MVRV closely tracks aggregate market prices. This is because the realised value of the network moves flat after early 2018 (see Figure 2). As a result, the MVRV is primarily linked to the current market value of the network, which in turn is ultimately determined by the BTC market price.

One comment is in order. Similar to the NVT, the MVRV does not tend to lead the dynamics of BTC prices over time. That is, the MVRV is of limited used as a predictor and therefore as a pure trading signal when used by itself. Nevertheless, the fact that the MVRV correlates with price dynamics makes it a useful indicator of underlying market trends.

Network-Value-to-Metcalfe’s-Law ratio

The number of active addresses is a measure that tracks the unique number of individual BTC addresses which either send or receive BTC within a given time period. In this respect, the number of active addresses represents an effective way of measuring investor demand and fundamental user interest in using BTC. It is therefore closely related to BTC’s long-run value.

The so-called Network-Value-to-Metcalfe’s-Law (NVML) ratio can be computed using this:

The Network Value is calculated as the total dollar value of all circulating units of a given BTC, and Active Addresses is measured as the unique individual BTC addresses which transact in BTC. This ratio makes use of the well-known Metcalfe’s Law, which states that the value of a network is proportional to the square of the size of the network. The number of BTC active addresses itself is steadily increasing.

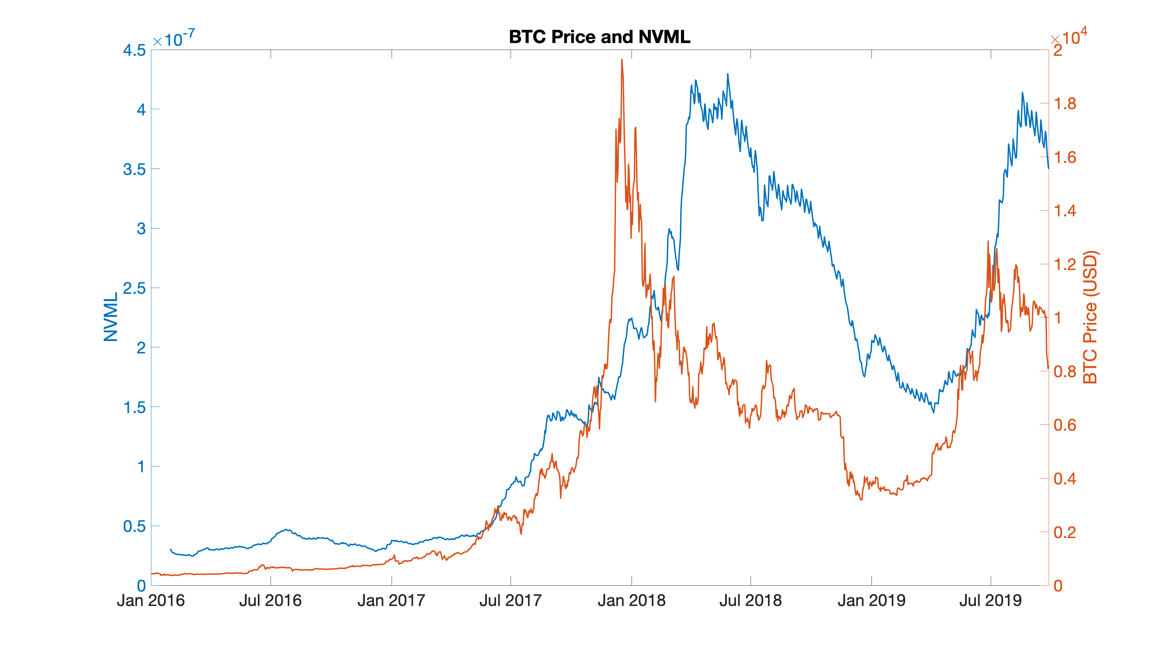

Figure 4: BTC Price and NVML

Figure 4 shows the NVML against BTC prices in USD. The ratio tracks closely the dynamics of the BTC price, although with a substantial lag in the aftermath of the bubble burst in early 2018. The ratio seems to capture fairly accurately the dynamics of BTC network valuation as a function of fundamental interest from investors.

One comment is in order. Quantifying the strength of network effects is a rather difficult task. This is because the exact marginal value of an additional participant to the network is not time-invariant (i.e. it can change over time). Some existing evidence shows that the Metcalfe’s law, being a square function of the network’s participants, does not effectively represents the strength of a network.

In this respect, the addition of a network participant increases the aggregate value of the network in a non-linear fashion. In particular, the value of each additional connection in the network begins to increase after a given threshold value, where the latter is network-specific. As a result, the NVML ratio, although instructive, should be taken with a grain of salt.

Exchange vs On-chain trading volume

There is a clear distinction between trading volume and transaction volume. The former typically refers to the amount of trading that takes place on regular exchanges, (e.g. Kraken, Coinbase, Poloniex, Bitstamp, Binance, etc.). Such activity is implemented off-chain, that is, transactions are normally mediated by the exchange and no validation from the network is required. Transaction volume, on the other hand, refers to on-chain transactions - those that are settled and validated directly on the blockchain for a fee.

Intuitively, on-chain transactions tend to reflect the activity implemented by real users of BTC, that is, those that effectively use BTC either as a store of value or as a method of payment. We call these “fundamentals”. On the other hand, off-chain transactions on exchanges tend to reflect trading activity by short-term speculators who aim to profit from price changes on BTC pairs against other cryptocurrencies or regular fiat currencies.

The fact that these two concepts reflect different trading motives may be seen in the dynamics of prices. For instance, increased trading volume with respect to aggregate BTC transactions may push prices up in a bubble-like trajectory.

For this reason, one indicator that market participants often look at is the Volume Ratio:

Figure 4: BTC Price and Volume Ratio

Figure 5 shows the dynamics of this ratio for BTC. Contrary to conventional wisdom, there is no strict relationship between the relative amount of trading activity on exchanges and price dynamics. The Volume Ratio and the BTC price share a common trend with the price run-up in late 2017, and then diverge in their timings around the the bubble burst of early 2018. Although it may not be profitable to build a short-term trading indicator on the Volume Ratio alone, it may be useful to look at it to navigate the market trend for BTC from a macro perspective.

Concluding Remarks

A variety of indicators have been proposed based on on-chain transaction volume. These indicators are primarily based on the assumption that on-chain transactions tend to reflect (1) the fundamental value of BTC and cryptocurrencies more generally, and (2) those who execute transactions on-chain are less prone to speculation. Although these two assumptions can be put into question from a theoretical perspective, the analysis on this report show that indeed on-chain transactions, coupled with market value, number of active addresses, and the trading volume on regular exchanges could represent valuable information to navigate market trends on BTC, if anything from a macro perspective.